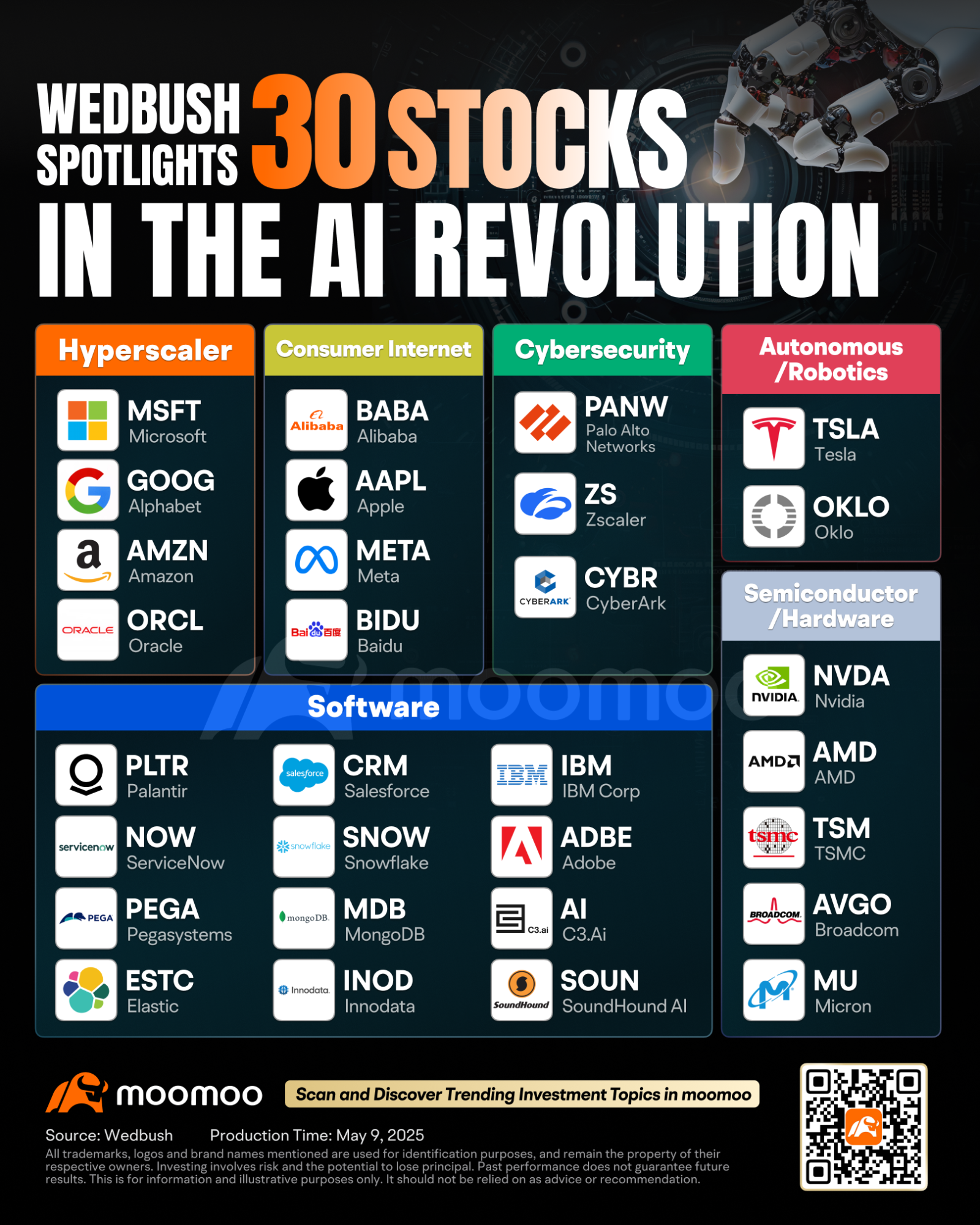

Dan Ives AI Stock Picks and Tech Upside

You are trying to decide whether this AI rally still has room to run, or whether the easy money is already gone. That is why Dan Ives AI stock picks are getting so much attention right now. The Wedbush analyst argues that tech stocks could have another 12 percent to 15 percent upside, driven by AI spending, cloud demand, and a broader belief that large-cap tech still has earnings power the market has not fully priced in.

That matters because plenty of investors are stuck between two bad choices. Chase momentum too late, or sit in cash while the biggest names keep climbing. Look, analyst calls alone should never drive a portfolio. But when a longtime tech bull puts real numbers on upside and names specific winners, it is worth breaking down what is signal and what is noise.

What stands out

- Dan Ives sees another 12 percent to 15 percent upside in tech stocks, even after a strong run.

- AI remains the core thesis, especially for companies tied to chips, cloud infrastructure, and enterprise software.

- Mega-cap leaders still dominate, which suggests the market is rewarding scale, data, and capital spending capacity.

- You should separate the narrative from the numbers, because not every stock with an AI label deserves the same premium.

Why Dan Ives AI stock picks matter now

Ives has spent years covering the biggest names in tech, and he tends to lean bullish. That does not make him wrong. It means you should read his call with the right frame.

His central case is simple. AI is pushing a new spending cycle across semiconductors, hyperscale cloud platforms, cybersecurity, and software. If companies keep buying infrastructure and tools to build AI products, the winners are not obscure startups. They are the large, cash-rich firms selling the picks and shovels.

AI is no longer a side story for tech investors. It is the spending engine many bulls think can support higher valuations.

That is the key point. A 12 percent to 15 percent upside target is not really about sentiment alone. It depends on revenue growth, margins, and capital expenditure translating into durable earnings.

Which Dan Ives AI stock picks fit the thesis

Based on Ives’ public AI commentary and recurring Wedbush themes, the names most tied to this view usually include Nvidia, Microsoft, and other large platform players. Sometimes the case extends to Palantir, Apple, and selected software names, depending on product traction and enterprise demand.

Nvidia and the AI infrastructure trade

Nvidia sits at the center of almost every bullish AI call for one reason. Demand for GPUs, networking, and data center gear has been massive, and rivals still have not closed the gap. If you think AI spending holds up, Nvidia remains the cleanest direct bet.

But price matters. Great business, expensive stock. That tension is real.

Microsoft and enterprise AI adoption

Microsoft has a stronger all-weather case because it blends cloud, productivity software, enterprise relationships, and OpenAI exposure. Azure growth and Copilot adoption are the pieces investors watch most closely. If AI becomes part of daily office work rather than a flashy demo, Microsoft could keep compounding.

Honestly, that is why many pros prefer it to more speculative AI names. It has a huge installed base and less binary risk.

Other likely beneficiaries

- Amazon, because AWS remains a core AI infrastructure platform.

- Alphabet, because it has the models, cloud business, and distribution to monetize AI at scale.

- Palantir, if enterprise and government AI deployments keep expanding.

- Apple, if on-device AI features drive an upgrade cycle and services growth.

Think of it like a basketball team. Star power matters, but the teams that keep winning usually control the boards, pace, and defense. In AI investing, infrastructure, distribution, and customer lock-in are those basics.

How much of the 12 percent to 15 percent upside is realistic?

That depends on three things.

- Earnings growth. If quarterly results keep beating expectations, the market can justify richer multiples.

- AI spending durability. If cloud providers and enterprises keep opening their wallets, the thesis holds.

- Interest rates and macro pressure. High-growth tech still reacts hard to Treasury yields and recession fears.

So, is 12 percent to 15 percent upside realistic? Yes, but not automatic. The market has already priced in a lot of good news, which means even strong companies can get hit if guidance slips.

This is where investors get sloppy.

They hear “AI” and assume every stock tied to the theme deserves a premium. It does not. Some firms have real demand and pricing power. Others have slide decks.

What to check before buying Dan Ives AI stock picks

If you are using this call as a research starting point, focus on evidence instead of excitement. Ask a few basic questions before you buy.

1. Is AI revenue real or still theoretical?

Listen to earnings calls and look for booked revenue, backlog, paid users, or disclosed customer wins. Vague references to “strong interest” do not count.

2. Can the company fund the AI race?

Training models and building data center capacity is expensive. Big balance sheets matter here (maybe more than many retail investors want to admit).

3. Is valuation already stretched?

A great company can still be a poor entry point. Compare forward price-to-earnings ratios, free cash flow trends, and expected growth against peers.

4. What breaks the thesis?

You need an exit view before you buy. That could be slowing cloud growth, weaker margins, regulatory pressure, or signs that customers are cutting AI budgets.

The risk Dan Ives bulls should not ignore

The biggest risk is not that AI disappears. It is that expectations outrun business reality. We have seen this before in tech cycles, where a real trend gets wrapped in inflated forecasts and the market punishes even minor disappointments.

There is also concentration risk. Much of the market’s recent gain has come from a small cluster of mega-cap tech names. If leadership narrows even more, portfolios can look diversified on paper while being heavily tied to the same AI trade.

Strong themes can carry stocks for months. Earnings, margins, and guidance decide what happens next.

How to use Dan Ives AI stock picks without chasing hype

You do not need to copy an analyst’s favorite names tick for tick. A smarter move is to sort the space into tiers.

- Core AI leaders. Companies like Microsoft and Nvidia with clear revenue exposure.

- Platform enablers. Firms like Amazon and Alphabet that can monetize AI through cloud and distribution.

- Higher-risk specialists. Names with more upside, but more valuation and execution risk.

Then decide what role each stock plays in your portfolio. Long-term compounder. Tactical momentum trade. Watchlist candidate. Very different jobs.

And ask yourself one blunt question. Are you buying because the business is getting stronger, or because the chart went up last month?

What comes next for AI stocks

Ives may be right that tech has more room to climb. The broad setup is still favorable if AI spending stays firm and the largest platforms keep posting solid numbers. But the next leg higher will probably be harder won than the last one.

The easy phase of the AI trade was spotting the obvious winners early. The next phase is stricter. You need to track earnings quality, customer adoption, and valuation discipline. That is less fun than chasing headlines, sure. It is also how you avoid paying top dollar for yesterday’s story.

If you are building around Dan Ives AI stock picks, start with the companies turning AI demand into cash, then watch the next two quarters like a hawk. That is where the real answer will show up.