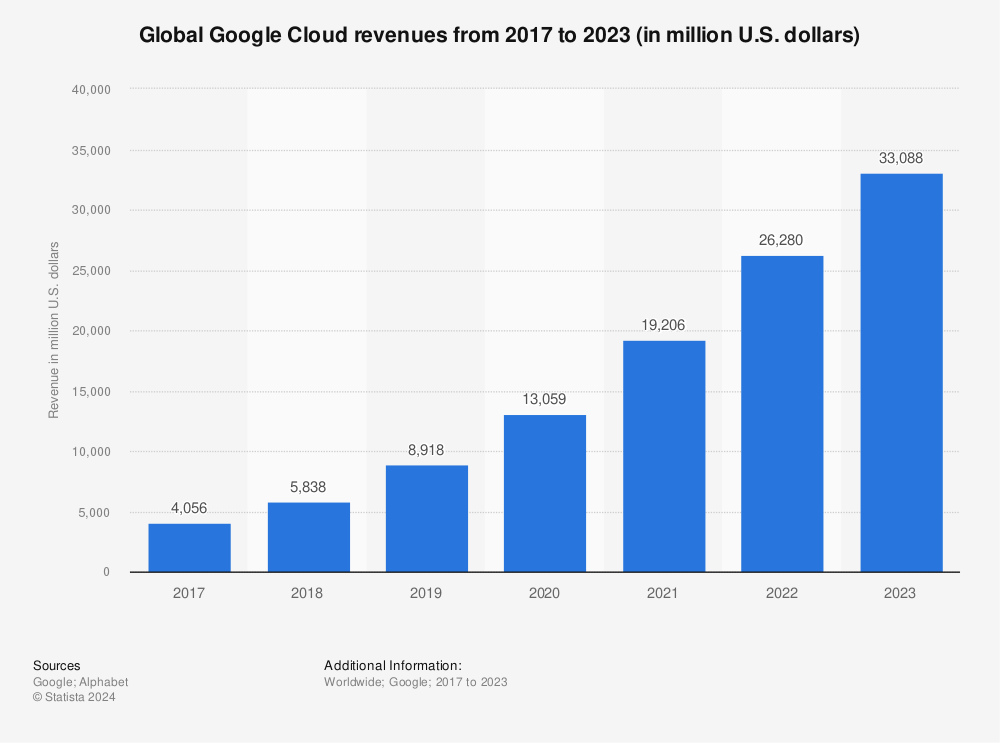

Google Cloud Revenue Hits $20B Amid Capacity Limits

If you track cloud infrastructure, one number jumps off the page. Google Cloud revenue has crossed $20 billion in a quarter, a marker that shows just how fast demand for cloud and AI infrastructure keeps rising. But there is a catch, and it matters. Google says growth was held back by capacity constraints, which means demand ran ahead of available compute, data center buildout, or both. For customers, that can affect pricing, access to GPUs, and deployment timelines. For investors, it raises a sharper question. Is Google leaving money on the table while rivals race to add supply? I have covered enough cloud earnings cycles to know this pattern is familiar. Demand is loud. Supply is stubborn. And right now, the bottleneck may be as telling as the revenue milestone itself.

What stands out

- Google Cloud revenue topped $20 billion, a fresh scale marker for the business.

- Google said growth was limited by capacity constraints, signaling demand outpaced supply.

- AI infrastructure demand, especially for compute-heavy workloads, is likely a major driver.

- Capacity limits can shape customer onboarding, pricing pressure, and future capital spending.

Why Google Cloud revenue matters now

Crossing $20 billion is more than a nice headline. It puts Google Cloud in a smaller club of hyperscale businesses with enough size to influence enterprise IT budgets, chip supply chains, and AI platform adoption.

Look, cloud revenue at this level tells you two things at once. First, the core business has real weight. Second, AI demand is no side show anymore. It is now tied directly to how much infrastructure these companies can put into the market.

Google is not saying demand is soft. It is saying the pipes are full.

That distinction matters. A slowdown caused by weak customer spending is one story. A slowdown caused by too little capacity is another, and usually the market prefers the second version because it suggests future revenue can still be pulled forward once supply improves.

What does capacity constrained growth actually mean?

Companies often use careful language on earnings calls, so it helps to translate this into plain English. If Google says growth was capacity constrained, it usually means customers wanted more cloud services than Google could deliver in the period, especially for high-demand resources like GPUs, TPUs, networking, storage, or data center power.

And yes, power may be part of the story. Across the cloud sector, data center expansion now depends on land, permits, electricity, cooling systems, and server delivery. Building cloud capacity is starting to look a bit like building a stadium. The money matters, but the real holdup is often steel, concrete, permits, and access roads.

That has a few likely effects:

- Large AI customers may wait longer for new capacity.

- Google may prioritize strategic accounts over smaller buyers.

- Revenue recognition gets delayed, even when customer demand is real.

- Capital spending pressure stays elevated as Google tries to catch up.

That bottleneck is expensive.

Google Cloud revenue and the AI infrastructure race

The obvious backdrop here is generative AI. Training and running large models burns through huge amounts of compute. Enterprises also want managed AI services, model hosting, databases, security layers, and data pipelines that sit on top of that compute. So a cloud provider is no longer just selling storage and virtual machines. It is selling access to scarce industrial-grade compute.

Google Cloud revenue is rising at a moment when Amazon Web Services, Microsoft Azure, and Oracle are all pushing the same message. Demand for AI services is strong, but supply is tight. That makes this less of a Google-only issue and more of an industry-wide stress test.

Why Google may have a real opening

Google has a few assets that fit this moment well. It has deep AI research roots, custom chips through TPUs, and a global cloud footprint. It also has a stronger story to tell around data analytics, Kubernetes, and model tooling than it did a few years ago.

But here is the hard truth. Good technology does not help if customers cannot get the capacity they need on time. Enterprise buyers tend to remember delays.

What customers should watch next

If you run cloud procurement, architecture, or AI deployment plans, this kind of earnings disclosure is useful. It gives you a read on where friction may show up next quarter.

- Ask about GPU and accelerator availability before you lock project timelines.

- Check whether your workloads can shift across regions if one area is tight.

- Review contract terms around reserved capacity and committed spend.

- Compare managed AI offerings against raw infrastructure if you need faster access.

- Press vendors on delivery windows, not just list prices.

Honestly, this is where glossy AI demos meet physical reality. If your vendor cannot provision compute, the roadmap slides.

What investors should take from Google Cloud revenue trends

Investors usually like demand-driven constraints more than demand weakness, but they should not ignore the trade-offs. Capacity shortages can support a bullish long-term view while still hurting near-term execution. Both can be true.

Questions worth asking include: How fast can Google add data center and accelerator capacity? Will operating margins hold up as spending rises? And can Google convert pent-up demand into revenue quickly enough before rivals scoop up workloads?

There is also a competitive angle. Microsoft has leaned hard into OpenAI-related demand. Amazon still has enormous enterprise reach. Oracle has become a louder voice in AI infrastructure than many expected. So if capacity stays tight across the market, every provider will try to steer limited supply toward the biggest or stickiest customers.

Is this a temporary ceiling or a longer bottleneck?

That is the real question, isn’t it?

Short-term constraints are common in periods of fast demand expansion. The bigger issue is whether this becomes structural. If power access, advanced chip supply, and data center construction remain constrained for several years, then cloud growth may increasingly depend on who can build fastest rather than who can sell best.

For Google, that would shift the challenge from product positioning to industrial execution. Different skill set. Different risks. And it may help explain why cloud earnings now sound as much like utility planning as software sales.

Where this leaves Google Cloud

Google Cloud passing $20 billion is a strong signal that the business has entered another tier. Still, the more interesting signal is the one underneath it. Demand appears strong enough that supply is the limiting factor.

If Google can add capacity fast and keep enterprise customers close, this could set up more upside in future quarters. If it cannot, rivals will be happy to step in. The next phase of the cloud fight may hinge less on flashy model launches and more on who can pour concrete, secure power, and ship compute at scale.