IBM vs Qualcomm AI Stock: Which Buy Looks Better Now?

You want AI exposure, but you do not want to pay any price for the story. That is the problem with many popular names right now. A lot of AI stocks still trade on hope, and hope can get expensive fast. The IBM vs Qualcomm AI stock debate matters because these two companies offer very different ways to play the same theme. One leans on enterprise software, consulting, and infrastructure. The other rides AI demand through smartphones, edge devices, and chips.

Zacks recently compared the two, and the contrast is sharp. IBM brings steadier cash flow and a slower, more mature profile. Qualcomm offers a more cyclical business, but it has a direct line into on-device AI, which could become one of the more practical corners of the market. So which stock deserves your money now?

What stands out right away

- IBM offers a steadier AI story tied to enterprise demand, hybrid cloud, and recurring software revenue.

- Qualcomm has more torque if on-device AI in phones, PCs, and edge hardware expands faster than expected.

- IBM looks like the more defensive pick. Qualcomm looks like the more aggressive one.

- Valuation, earnings revisions, and business mix matter more here than AI headlines.

IBM vs Qualcomm AI stock: What are you really buying?

Look past the AI label for a minute. These are not two versions of the same company.

IBM sells a mix of software, consulting, automation, and infrastructure. Its AI push runs through Watsonx, enterprise data tools, and services that help big companies deploy AI in real operations. That matters because many firms do not just need models. They need governance, integration, and compliance work too.

Qualcomm is a semiconductor and wireless giant. Its AI case depends heavily on edge AI, meaning AI tasks processed on devices instead of in distant data centers. Think premium smartphones, AI PCs, automotive systems, and industrial hardware. If that trend keeps building, Qualcomm sits in a good spot.

Here is the real split: IBM sells AI as a business tool. Qualcomm sells the hardware layer that helps AI run closer to the user.

That difference shapes everything from growth rates to risk.

Why IBM still has a serious AI case

IBM’s AI business fits how large companies actually buy technology

Big enterprises rarely swap out core systems overnight. They add tools in stages, test them, then scale what works. IBM understands that buying pattern better than most vendors, and that gives it an edge with cautious corporate clients.

Its hybrid cloud and AI strategy is built for large organizations with messy data, old systems, and strict rules around privacy. That is not flashy. It is useful. And useful tends to age well.

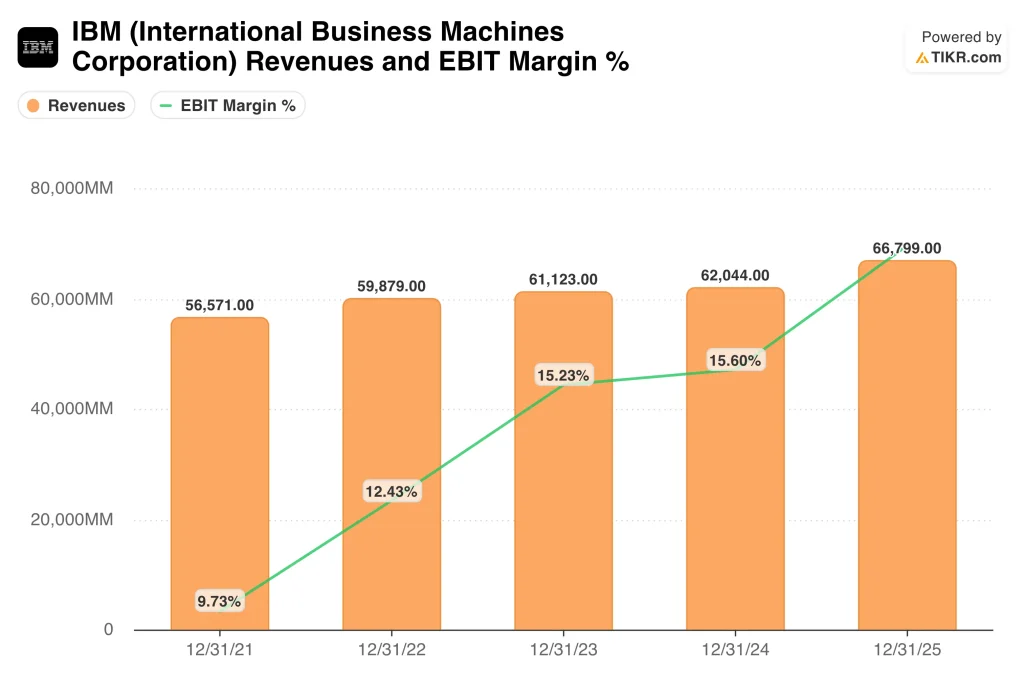

IBM has a steadier revenue mix

Software and consulting can produce more predictable results than consumer device cycles. IBM also has a long history with large accounts, which helps when companies want one vendor to help stitch systems together.

Honestly, this is why IBM keeps showing up in serious investor conversations. It is not the loudest AI stock, but it may be one of the more durable ones.

Steady can win.

What could hold IBM back

The obvious problem is speed. IBM is unlikely to post the kind of explosive growth that sends momentum investors into a frenzy. It also faces stiff competition from Microsoft, Amazon, Google, and Oracle in enterprise AI and cloud services.

And there is another issue. Consulting-heavy AI revenue can be solid, but it does not always scale the way software investors want. Think of it like architecture versus real estate. One business designs the system. The other collects rent at scale.

IBM vs Qualcomm AI stock: Why Qualcomm may have more upside

Qualcomm is tied to on-device AI, and that trend looks real

Why send every AI task to the cloud if the device in your hand can do part of the work faster, cheaper, and with better privacy?

That question sits at the center of Qualcomm’s pitch. Its Snapdragon platforms are already embedded in smartphones and are expanding into PCs and automotive systems. If AI features become standard on premium devices, Qualcomm could benefit from both unit demand and richer chip content.

This is where the stock gets interesting. On-device AI is not just a buzz phrase. It addresses latency, battery efficiency, and privacy concerns. Those are real product issues, not marketing fluff.

Qualcomm also has more cyclical snap

If handset demand improves and AI-enabled upgrades accelerate, Qualcomm can move faster than IBM. Chip stocks often react sharply when the cycle turns. That can be great on the way up and painful on the way down.

And yes, the volatility is part of the package.

What could hold Qualcomm back

Its dependence on smartphones still matters, even as it expands into automotive and PCs. Consumer hardware demand can weaken quickly, and chip competition never sits still. Apple, MediaTek, Nvidia, AMD, and Intel all shape the broader environment in different ways.

Qualcomm also faces the usual semiconductor risks, including inventory swings, pricing pressure, and customer concentration. If you buy it, you are accepting a bumpier ride.

Which stock looks stronger on valuation and risk?

Zacks framed the matchup through the lens investors actually use: growth, valuation, and earnings outlook. That is the right approach. AI stories matter, but numbers still decide returns over time.

IBM tends to appeal when you want quality, cash generation, and less drama. Qualcomm tends to appeal when you want more upside tied to a hardware cycle and the spread of edge AI.

- If you want a lower-volatility AI stock, IBM is the cleaner fit.

- If you want a higher-upside AI stock and can handle cyclicality, Qualcomm may be more attractive.

- If your time horizon is short, sentiment and earnings revisions could matter more than the long-term AI thesis.

- If your time horizon is long, business mix and execution matter most.

Here is my read after years of watching tech cycles. The market often overpays for the loudest AI names and underestimates the companies solving boring enterprise problems. But it also misses device shifts until they are obvious. IBM and Qualcomm each exploit one of those blind spots.

So, which AI stock is the better buy now?

If you force me to choose one today, IBM looks like the better buy for most investors. The reason is simple. Its AI story is easier to connect to enterprise spending, recurring revenue, and operational demand that does not rely on a consumer upgrade wave. In a shaky market, that profile usually holds up better.

But for investors who can stomach more swings, Qualcomm may offer the bigger payoff if on-device AI becomes standard across premium phones, PCs, and connected systems. That is a real if, though. Not a sure thing.

(And that distinction matters more than the headline.)

What I would watch next

Do not just watch press releases. Watch proof.

- For IBM vs Qualcomm AI stock, track earnings revisions and forward guidance.

- For IBM, look for software growth, Watsonx adoption, and margin trends in its AI-related offerings.

- For Qualcomm, watch handset demand, AI PC traction, and expansion in automotive revenue.

- For both, pay attention to whether AI revenue is recurring, sticky, and profitable, or just attached to broad marketing claims.

The smarter bet is the one with a cleaner path from AI excitement to actual cash flow. Right now, IBM has the sturdier bridge. Qualcomm may still have the faster car. Which matters more to you over the next two years?