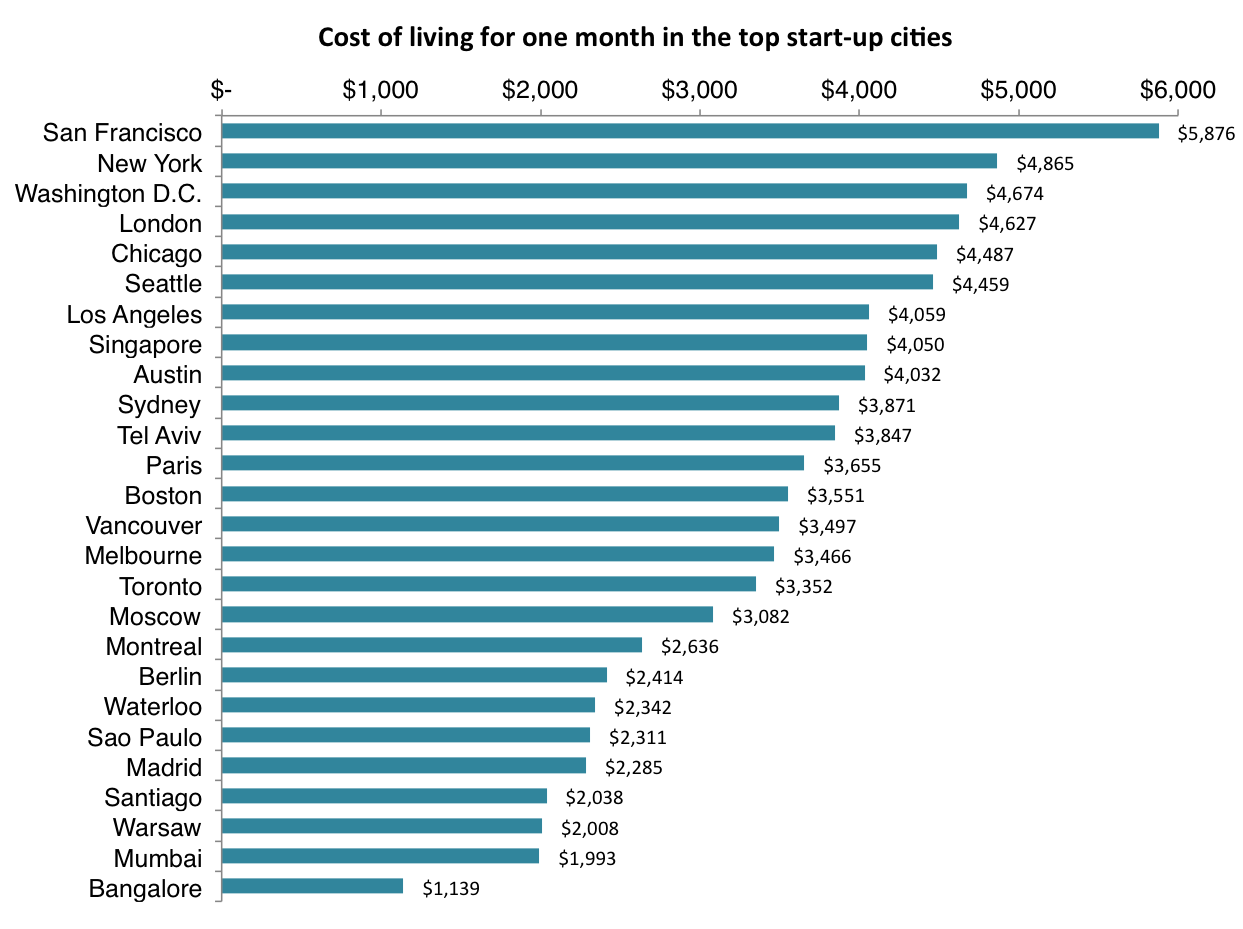

Lowering the Cost of Living Is the Next Startup Play

People are done paying more for less. Rent keeps climbing, groceries bite harder, and childcare can feel like a second mortgage. That is why cost of living startups matter now. They do not win by chasing flashy features. They win by taking pressure off the monthly budget, line item by line item.

Andrew Yang’s view is simple enough to feel obvious, which is usually a sign that the market has been missing it. If a startup can shave real dollars off housing, food, healthcare, transport, or utilities, you do not need a giant pitch deck to explain the value. You can show the bill. And that is a very different kind of product story.

What cost of living startups can actually do

- Cut recurring expenses through better pricing, pooling, or automation.

- Reduce waste in categories where people overpay because the system is messy.

- Make access easier for services that already exist but are hard to use.

- Use data and software to expose cheaper options fast.

- Build trust by showing savings in plain numbers, not glossy promises.

Why the mainKeyword fits this moment

The startup market has spent years rewarding software that improves work. Good. But that leaves a huge gap. Most households do not feel rich because their productivity app runs smoothly. They feel pressure because fixed costs keep rising faster than paychecks.

That is the opening. Not a theoretical one. A practical one. When people ask where the next serious startup wave comes from, the answer may look less like entertainment and more like a bill reduction engine.

“If you can save a family $200 a month, you have built something that people will talk about at the dinner table.”

Where founders can find real savings

Look at the categories that eat budget first. Housing, healthcare, food, transportation, and child care. These are not glamorous markets. They are also enormous, stubborn, and full of friction.

Housing

Housing is the toughest one, because supply is political and slow. But software can still help. Tools that simplify roommate matching, short-term subleasing, permit workflows, rent negotiation, or energy management can trim costs without pretending to solve zoning in one sprint.

Food and household basics

Groceries are a daily tax on attention. Apps that compare store prices, reduce delivery fees, or improve bulk purchasing can save money if they avoid hidden fees. The analogy here is a kitchen knife set. You do not need a thousand gadgets. You need the one tool that cuts cleanly.

Healthcare and insurance

Healthcare remains a maze. Startups can help people compare bills, find lower-cost prescriptions, negotiate charges, or route care to cheaper settings. That is where software gets useful in a very human way. It helps people ask better questions before they sign away money they do not have.

And yes, this space is crowded with weak ideas. A consumer app that merely tracks spending is not enough. Why would anyone switch for a prettier dashboard?

What makes this different from old budgeting apps

Old budgeting tools mostly tell you where your money went. Cost of living startups should change where the money goes in the first place. That is the real shift.

- They must find savings, not just classify spending.

- They need to work inside painful, real categories.

- They have to prove value quickly, or people will churn.

- They should price themselves so the savings are obvious.

That last point matters more than founders admit. If your product saves $40 and costs $35, the customer will not feel relief. They will feel tricked. The economics have to be clean.

What investors should look for

Investors often chase markets with clean software margins. Fine. But the next big opening may come from messy sectors where the payoff is immediate and easy to verify. A product that cuts a monthly bill has a clearer retention story than one that only improves workflow.

Look for three signals. First, the user can measure savings in under a month. Second, the product fits an essential budget category. Third, the company can grow without depending on hype or regulatory luck. If those three are missing, the thesis gets shaky fast.

Why this idea has staying power

Cost pressure is not a fad. It moves with interest rates, wages, housing supply, and family budgets. That makes it more durable than the usual startup trend cycle. One year it is social audio. The next it is AI wrappers. But the need to spend less never leaves.

That is what makes this theme feel seismic, even if the products themselves look plain. The best ones will not sound sexy in a demo video. They will sound useful at 7 p.m. when a parent is checking a bank balance before payday.

Founders should stop asking what looks futuristic and start asking what makes life cheaper. That is the more interesting race. Who builds the first product that people keep because it pays for itself every month?

Where the next move happens

The next strong startup may not change the way you live online. It may change what stays in your account after rent, food, and bills. That is a harder business to build, but a better one to own.

And if Yang is right, the winners will not be the loudest companies in the room. They will be the ones that make your budget breathe. So what category do you think is next, and who is ready to attack it with discipline instead of hype?