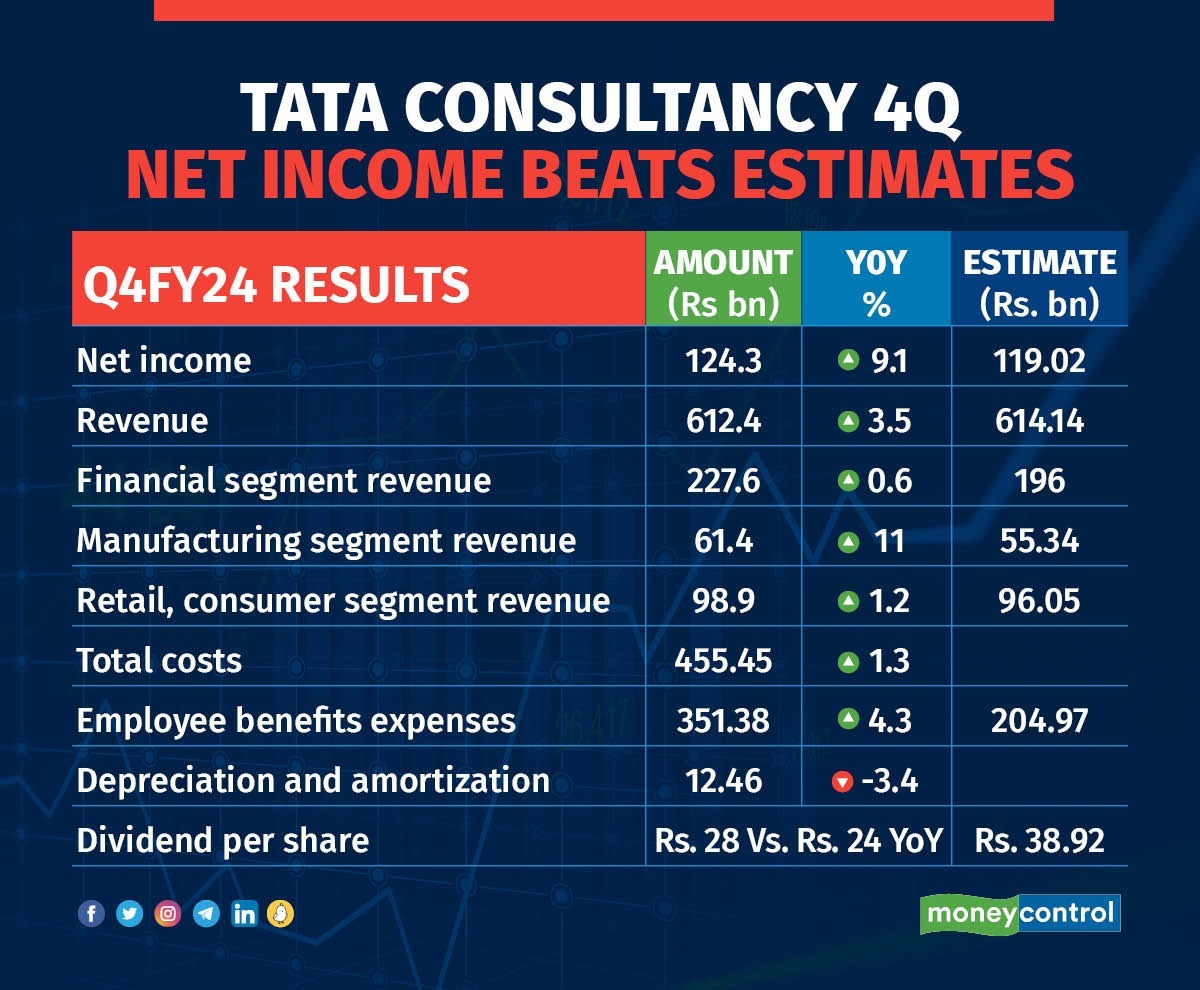

TCS Q4 earnings: what investors should watch on April 9

Investors eye TCS Q4 earnings because margin stability, the next dividend cue, and AI traction all land on April 9. The mainKeyword here is TCS Q4 earnings, and it matters now: global tech budgets are tight, clients push for automation, and India’s IT bellwether sets the tone for the sector. You need to know how deal wins, pricing, and utilization hold up, and whether the promised AI-led efficiency actually shows up in numbers. I have covered this beat long enough to know that headlines hide the real tells—cash discipline, client churn, and hiring trends. Think of it like scouting a cricket side before a big tour: form, bench depth, and captaincy signals decide the scorecard.

What to watch in TCS Q4 earnings

- Revenue growth mix: BFSI and retail softness vs. emerging cloud deals.

- Operating margin bands and onsite-offshore shift.

- Deal TCV disclosures and pricing sticks vs. renewals.

- Attrition and subcontractor spend as efficiency gauges.

- Dividend per share and payout consistency.

Why the dividend signal matters

Cash returns still matter.

TCS has a reputation for steady payouts, but a wobble in free cash flow or a lower interim dividend would hint at caution. I look for payout ratio discipline and whether working capital balloons. If the board keeps the line, it tells you the business can fund AI bets without starving shareholders.

“A tight payout with stable margins is the cleanest tell that AI spending is not cannibalizing returns.”

TCS Q4 earnings and AI credibility

AI talk is easy. Delivering code productivity gains is not. Watch for quantified efficiency metrics—cycle time cuts, improved utilization, and fewer subcontractor hours. Any mention of proprietary models should come with client adoption numbers, not just press-friendly claims. Remember, AI in services is like switching from pace to spin mid-innings: it only works if the field is set right.

Client signals to track

- Are North America clients expanding pilots to production?

- Do EU regulated industries cite compliance-ready AI wins?

- Is pricing holding when AI automation trims seat counts?

Deal pipeline and hiring tell their own story

Net hiring and campus offers show if management expects demand to rebound. A sharp drop hints at cautious pipelines. But a modest add paired with higher training spend would mean they are reskilling for AI-heavy work. Ask yourself: would you pay a premium if delivery teams are thin?

Risks that could spoil the quarter

Currency swings can shave margin. Client decision delays could push revenue into the next quarter. Any uptick in receivables days would signal stretched clients. Here’s the thing: one soft quarter is survivable, but two in a row erodes pricing power.

How I would read the call

Listen for specifics: named client wins, quantified AI benefits, and clear capital allocation. Skip the buzzwords. If management ducks direct questions on margin levers, treat that as a red flag. If they outline concrete tooling rollouts and training numbers, that is a positive. Investors should press on whether AI-driven productivity will flow back to clients or stay on the P&L.

Next move for investors

If TCS posts stable margins, steady dividend, and credible AI uptake, staying invested looks rational. A miss on any two of those three should trigger a rethink. So, will April 9 confirm resilience or expose softness?