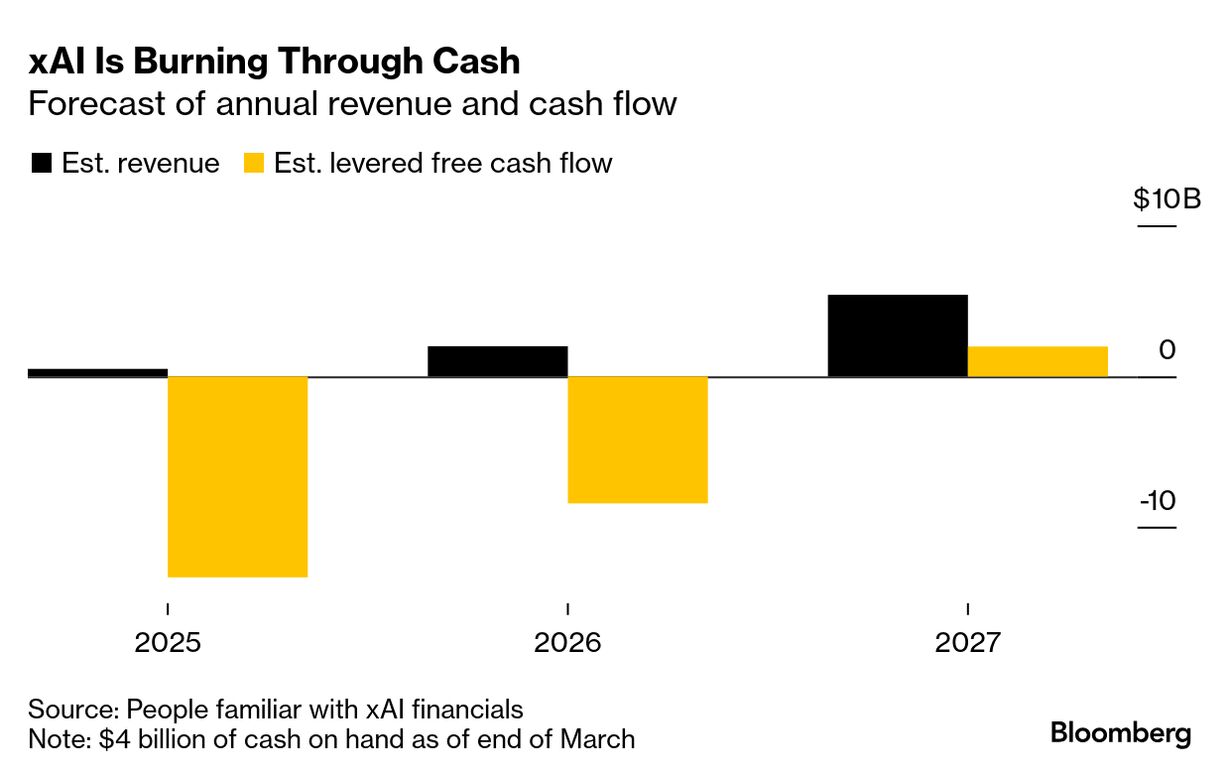

xAI Burn Rate Explained

xAI burn rate is no longer a side note for people who track AI companies. It is the story. TechCrunch reported that xAI burned $6.4 billion last year, citing details tied to SpaceX’s IPO filing. That number matters because it shows how expensive the current AI arms race has become, especially for companies chasing frontier models, giant data centers, and custom infrastructure. If you are trying to judge whether xAI looks disciplined or dangerously stretched, the burn figure gives you a much cleaner signal than splashy product demos do. And it raises a basic question. How long can any AI company spend at this clip before revenue, outside financing, or both have to catch up?

What stands out right away

- xAI burned $6.4 billion in a single year, which puts it in the top tier of AI cash consumers.

- The spending likely reflects compute, data center buildout, and model training, not short-term excess alone.

- SpaceX’s filing offers unusual visibility into a private AI company that usually shares little financial detail.

- The bigger issue is durability. Can xAI turn massive capex and operating costs into a business with real margins?

Why the xAI burn rate is so high

Training and serving large language models is expensive at a scale that still shocks people outside the sector. GPUs cost a fortune. Networking gear does too. Then add power, cooling, land, facilities, engineers, data pipelines, and the cost of keeping inference fast enough for users who will not wait around.

Look, frontier AI is starting to resemble heavy industry more than software. The old startup playbook was small team, fast growth, and high gross margins. This looks closer to building a shipyard, then racing another shipyard to launch bigger vessels every quarter.

That helps explain why xAI burn rate is not a freak number. It is a signal of the market it chose to enter. Competing with OpenAI, Google DeepMind, Anthropic, and Meta means spending at their altitude, or getting left behind.

What the reported spending says about xAI’s strategy

Burn alone is not proof of failure. Sometimes it shows intent. xAI appears to be spending as if speed matters more than near-term efficiency, which makes sense if management believes the market will reward scale, model quality, and infrastructure control before it rewards profit.

That is a defensible bet, up to a point.

But investors should not confuse aggression with inevitability. Plenty of tech companies have spent huge sums to secure a strategic position, only to find that the market settled around lower-cost players, open models, or cloud providers with stronger balance sheets. AI is not immune to that pattern.

Big AI spending can buy time, talent, and compute. It cannot guarantee a moat.

xAI burn rate and the real cost of infrastructure

The cleanest way to read this story is through infrastructure. Model builders often talk like software companies, but their economics now depend on physical systems. NVIDIA chips, high-bandwidth memory, interconnects, racks, power contracts, and data center capacity are the non-negotiable pieces. Miss one, and the whole machine slows down.

And slow is deadly in this market.

That is why companies like xAI keep spending. If they delay infrastructure investment, they risk weaker training runs, slower product updates, and less capacity for inference as user demand grows. It is a bit like a Formula 1 team. The car matters, yes, but so do the engine, pit crew, telemetry, and track strategy. You do not win by funding only one part.

Where the money likely goes

- GPU and accelerator purchases or long-term commitments

- Data center construction and leasing

- Power, cooling, and networking infrastructure

- Research staff and specialized engineering talent

- Inference costs for live products such as Grok

What investors and operators should watch next

If you are evaluating xAI, the next question is simple. What offsets the burn? Revenue growth, strategic partnerships, debt capacity, equity financing, and infrastructure sharing all matter more now than broad claims about future AI demand.

Honestly, this is where AI coverage often gets too soft. People love to quote valuation marks. They spend less time asking whether the business underneath can absorb the operating load without endless capital raises.

Watch these signals:

- Revenue quality. Is xAI selling sticky enterprise products, consumer subscriptions, API access, or mostly promise?

- Gross margin direction. Are inference and model costs improving as scale grows?

- Capex intensity. Is spending tied to assets with lasting value, or to short-lived compute cycles?

- Funding mix. Equity is one thing. Debt against volatile AI economics is another.

- Product pull. Are users choosing Grok because it is better, or because it is bundled into a larger ecosystem?

Does this make xAI weak, or just early?

Both are possible. Early-stage leaders often look messy on the financials because they are buying position before the market settles. Amazon looked reckless to critics for years because it kept pouring cash back into logistics and infrastructure. The difference is that Amazon was building demand and operating systems in a market with clearer customer behavior.

xAI is building in a market where model leadership can fade fast, open-source alternatives keep improving, and buyers are still figuring out how much they will actually pay for AI over the long haul. That makes the xAI burn rate more than a headline. It is a stress test of the whole thesis.

What this means for the wider AI sector

xAI is not the only company spending hard. It is just one of the few where outsiders got a better look at the numbers. The broader lesson is that frontier AI is concentrating power around companies that can raise vast sums, secure chip supply, and tolerate years of financial pressure.

That could produce stronger products. It could also narrow the field.

For startups, the message is blunt. If you cannot outspend the giants, you need a sharper angle. Maybe that means vertical AI software, fine-tuned domain models, lower-cost inference, or tools that sit on top of foundation models rather than trying to replace them. Trying to beat the biggest labs at their own capital game is usually a losing hand.

The number behind the hype

TechCrunch’s report matters because it puts a hard figure under a very noisy AI narrative. A $6.4 billion annual burn tells you xAI is playing for scale, not caution. It also tells you the bill for frontier AI is still climbing, not easing.

If you are reading the sector with clear eyes, that is the takeaway. The winners may be brilliant model companies. Or they may be the firms that sell picks, shovels, power, and cloud capacity to everyone else. Over the next year, watch who turns spending into durable demand, because that is where the story gets real.